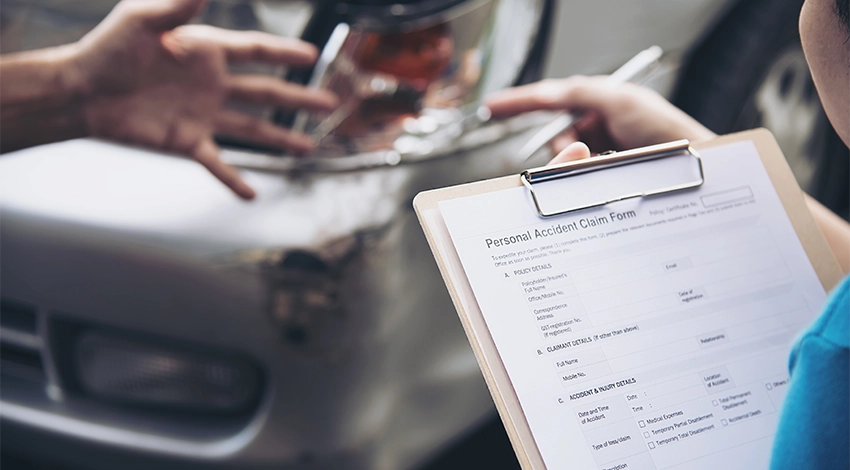

One of the most common questions among car owners in Azerbaijan is how CASCO insurance pricing works. Many people assume that the price is fixed, but in reality, it is calculated based on individual risk factors.

The main goal of CASCO pricing is to assess the risk profile of both the vehicle and the driver. The higher the risk, the higher the premium. This approach follows international risk-based pricing models used in insurance markets worldwide.

The market value of the vehicle is one of the most important factors. The more expensive the car, the higher the repair or replacement cost, which directly increases the insurance price.

The age of the vehicle also plays a role. Newer cars usually have higher repair costs, while older cars may have different risk dynamics depending on condition and usage.

Driver experience and insurance history are also key. Drivers with no accident history typically receive lower premiums, while high-risk drivers pay more.

The selected coverage level significantly impacts the price. More comprehensive packages cost more but provide broader protection. Limited coverage options may reduce the price but increase exposure to risk.

Deductibles also influence pricing. Accepting a higher deductible lowers the premium and balances cost with risk.

Rising repair costs and expensive spare parts have made CASCO pricing more dynamic. Insurance companies continuously adjust pricing based on market conditions.

CASCO insurance pricing varies depending on multiple factors. The best approach is to compare options and choose based on your personal risk profile.